Most enterprises don’t have a growth strategy problem. They have a growth architecture problem. The evidence is everywhere: well-resourced companies with sophisticated strategies that still can’t compound their growth. The reason is structural. They keep launching growth projects when what they need is a growth engine – a permanent, compounding system that converts market intelligence into high-conviction action at scale. This article breaks down what that engine looks like, why most organizations fail to build it, and what it actually takes to operate one.

Why Your Growth Strategy Is Structurally Broken

Enterprise growth strategies fail not because they are wrong, but because they are built on an architecture that cannot carry them. The modern growth engine has to be designed from the ground up – not bolted onto a planning cycle that was built for a more predictable era.

The mid-market paradox: too large to pivot, too constrained to hedge

Mid-market enterprises occupy the most strategically uncomfortable position in the economy. They have outgrown the reflexes of a startup but don’t have the balance sheet of a global conglomerate to place multiple simultaneous bets. The result is a specific kind of paralysis: too committed to the core to move fast, too resource-constrained to absorb a failed experiment.

This is the mid-market paradox, and it explains why so many capable leadership teams find themselves stuck. They are not short of ideas. They are short of a system for evaluating, sequencing, and scaling the right ones without jeopardizing the existing business.

The three market forces making the old playbook obsolete

Three forces are actively dismantling the assumptions on which most enterprise growth strategies were built.

The first is contextual fragmentation. Markets are no longer monoliths. Purchasing behavior is bifurcating sharply – premium segments demand highly specific experiences while others trade down aggressively. Growth now belongs to organizations that can map their offerings to specific customer contexts rather than mass-market averages. The customer you served three years ago is making decisions differently today.

The second is AI-driven asymmetric competition. Artificial intelligence and advanced analytics have decoupled competitive advantage from organizational scale. A lean, AI-native competitor can now bypass the traditional advantages of size – distribution reach, data volume, brand recognition – and compete with precision that incumbents cannot match through headcount alone. Speed and relevance have become structural requirements, not differentiators.

The third is the rising cost of a failed bet. Margin compression, supply chain volatility, and sustained macroeconomic uncertainty have raised the penalty for misallocated capital to levels that make the old “growth at all costs” posture genuinely dangerous. Leadership teams are right to move toward high-conviction deployment. The problem is that conviction requires a decision infrastructure most organizations haven’t built.

Why growth projects fail where growth engines succeed

A growth project has a sponsor, a timeline, and a budget. A growth engine has a permanent sensing layer, a decision architecture, and a compounding feedback loop. The distinction sounds abstract until you map the failure modes.

Projects stall when the sponsor moves on. Projects lose momentum when they hit the first organizational obstacle. Projects produce learnings that never get institutionalized. Engines, by contrast, are self-correcting systems. They get sharper with each cycle because the learning is embedded in the structure, not stored in a slide deck.

The Five Levers of Modern Enterprise Growth

A modern growth engine doesn’t operate on one lever. It requires five, working simultaneously across different horizons and customer relationships.

Contextual re-segmentation – solving for the job, not the demographic

The growth opportunity in most categories is hiding inside unmet jobs-to-be-done, not inside underserved demographics. Olipop and Poppi didn’t find whitespace by looking at who wasn’t drinking soda. They found it by identifying a specific job – functional refreshment without sugar guilt – that was completely unmet in the moments where people needed it. They re-segmented by context, not by customer profile.

For enterprise leaders, the question is whether your current segments are defined by historical data or by the precise problems your customers are trying to solve right now. Those are usually different questions with very different answers.

Customer equity maximization – your existing base as your highest-margin engine

The most efficient growth engine most enterprises have is already inside their existing customer relationships. Existing customers carry lower acquisition cost, higher data richness, higher trust, and higher lifetime value (LTV) than any new segment you can target. The strategic error most organizations make is investing more in reaching strangers than in maximizing the potential of their most loyal customers.

LEGO’s decade-long growth story is instructive. By re-engaging its adult fan community and expanding into co-creation platforms, physical experiences, and digital extensions, the company tripled its revenue – not by winning new demographics, but by deepening the total value delivered to people who already loved the brand. The LTV:CAC ratio on an existing customer is almost always more favorable than the acquisition math on a new one.

Revenue stream diversification – monetizing the edges of your core

The most resilient enterprises are building high-margin services and revenue models around their core products rather than simply extending those products. This means moving from linear sales into subscription, usage-based, or data-driven models. It means identifying where the data or capabilities that live inside the business can be monetized externally.

Uber’s evolution is the clearest proof of this logic at scale. Its logistics infrastructure – built to move people – turned out to be a platform for moving food and freight. Uber Eats, Uber Direct, and Uber Freight now represent nearly half of total bookings. The core product was not extended. The underlying infrastructure was re-monetized against adjacent jobs.

Distribution as competitive infrastructure – not logistics, but discovery

This is the reframe that most growth strategies miss entirely. Distribution is not a route-to-market question. It is an infrastructure question – one that determines whether the right message reaches the right person in the right context at all. Companies that treat distribution as a logistics function are ceding the most important competitive variable in a fragmented attention economy.

e.l.f. Beauty’s growth trajectory makes this concrete. The brand moved at the speed of culture by treating TikTok and creator ecosystems not as marketing channels but as discovery infrastructure. The product didn’t change. The distribution architecture changed – and with it, the entire competitive position.

The question every enterprise leader should be asking is not “which channels are we using?” but “which emerging distribution infrastructure would a well-funded competitor use to bypass our existing reach entirely?”

Business model evolution – from linear value chains to adaptive ecosystems

The final lever is the most structural. The companies building durable competitive positions are those transitioning from rigid, linear value chains into flexible, technology-powered ecosystems that can flex as market conditions shift.

Walmart’s evolution from brick-and-mortar retailer to omnichannel platform – anchored by Walmart Connect and Walmart+ – demonstrates how a legacy incumbent can build diversified, high-margin revenue streams without abandoning its core. The business model wasn’t replaced. It was made adaptive. That is a fundamentally different operation than simply launching new products.

Why Growth Stalls: Five Failure Modes You Can Engineer Out

The bottleneck in most enterprise growth programs is not insight – it is decision architecture. Companies have more data than they have ever had, and they are growing more slowly than they expected. The missing component is not another dashboard; it is a clear, accountable system for who decides what, with what data, by when.

These five failure modes explain why growth stalls in organizations that have no shortage of talent, capital, or strategic intent.

Insight lag – building strategy on yesterday’s signals

Most organizations learn too slowly. By the time a market shift has worked its way through surveys, quarterly reviews, and planning cycles, the window for a high-conviction response has often already closed. Forward-leading growth engines invest in behavioral analytics and AI-driven signal detection specifically to compress the gap between market change and organizational response. Attitudinal surveys describe what customers felt last quarter. Behavioral data shows what they are doing right now.

Aperture lock – how the core business cannibalizes the future

Leadership teams under pressure default to protecting what’s working. This is rational at the individual decision level and catastrophic at the organizational level. Aperture lock occurs when the core business systematically crowds out adjacent bets – not through explicit decisions, but through resource allocation, attention, and incentive structures that are all pointed at the status quo. The Three Horizons model is a useful diagnostic here: most organizations are over-invested in Horizon 1 optimization and structurally incapable of funding Horizon 2 exploration.

Activation gap – the graveyard between strategy and pilot

Strategy documents are not growth. The activation gap is the distance between a well-articulated opportunity and the first real-world experiment that tests it. Most enterprises are far better at producing strategic analysis than at deploying small-scale pilots quickly enough to generate evidence. The gap is rarely about capability. It is almost always about decision rights and risk tolerance at the mid-management layer.

Decision fog – when authority is unclear, growth stops

Decision fog is the most common and least discussed reason growth programs stall. When it is not clear who has the authority to act on an insight, approve a test, or kill a failing initiative, the organization enters a holding pattern. The data exists. The analysis exists. The will may even exist. But without clear ownership and decision rights, every growth initiative eventually becomes a committee problem – and committees are not growth engines.

Operating model drag – when the org rejects the innovation it commissioned

Most enterprise operating models are structurally optimized for the last wave of growth, not the next one. KPIs are calibrated for the existing business. Incentive structures reward the wrong behaviors. Budget cycles are too slow for the experimentation cadence that growth requires. When the organization’s internal systems are all pointed at the status quo, they will actively reject the behaviors that innovation demands – not out of malice, but out of structural coherence.

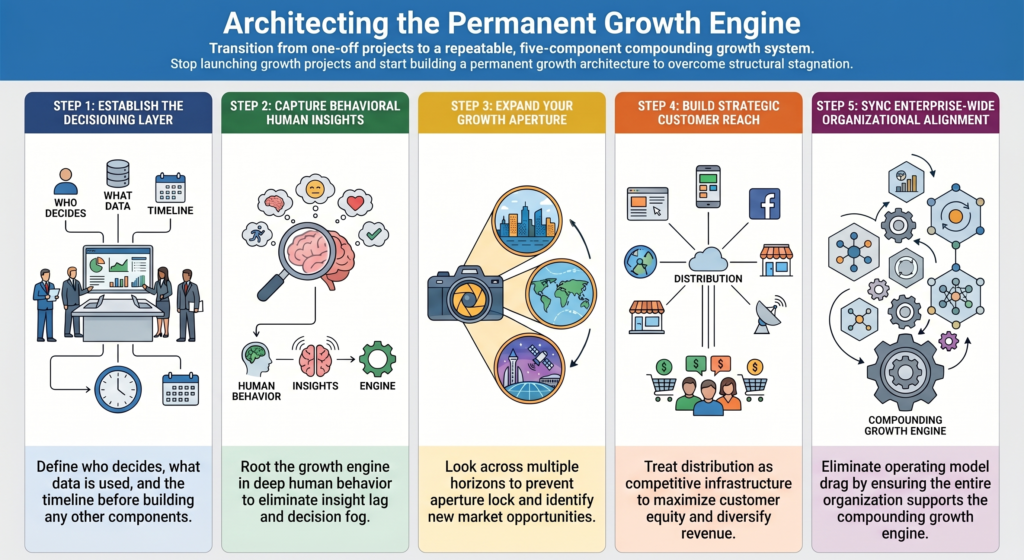

The Five Components of a Repeatable Growth Engine

A repeatable enterprise growth engine is built from five permanent components. Each one is infrastructure, not initiative.

Human insight – behavioral intelligence, not attitudinal surveys

The engine begins with a deep, continuous understanding of the specific frictions customers face and the jobs they are trying to complete. This is not a research function that runs annually. It is a live sensing capability that uses behavioral analytics, AI-driven micro-trend detection, and real-time sentiment monitoring to identify emerging shifts before they show up in the quarterly data. Growth occurs when a company can perceive market changes faster and more clearly than its competitors.

Growth aperture – replacing passion projects with horizon-spanning portfolios

The growth aperture component replaces the episodic, sponsor-driven project with a disciplined portfolio of bets across multiple horizons. It expands the strategic lens beyond the core business to include adjacent customer contexts, new service categories, and emerging value pools – including data-driven ecosystems and platform models. The mindset shift is from “what should we do next” to “what portfolio of bets gives us the highest probability of capturing value across all three horizons simultaneously.”

Customer reach – treating distribution as a strategic asset

Winning in a fragmented market requires treating distribution as a first-order strategic question, not an operational one. This means testing new channels and platforms with the same rigor applied to product development, using AI for hyper-personalization at scale, and building strategic partnerships that expand reach into contexts the core business cannot access alone. Distribution that is treated as infrastructure compounds. Distribution that is treated as a channel does not.

Decisioning layer – building decision infrastructure, not just data infrastructure

Most enterprises don’t have a data problem. They have a decision problem. The decisioning layer is the organizational mechanism that converts data into action: clear decision rights, AI-enhanced forecasting, rapid experimentation platforms, and unified data that actually reaches the people who need it at the moment they need to act. In an environment where speed of decision is a competitive variable, what an organization chooses to do – and how fast it commits – is more important than the quality of its analysis.

Organizing for growth – enterprise-wide capability, not departmental function

Sustained growth is not a marketing function or a strategy function. It is an enterprise-wide operating capability that requires dismantling the silos that slow down data and talent flow, aligning decision rights with growth priorities, and calibrating KPIs and incentives toward long-term value creation rather than short-term output. The growth flywheel only spins when insight, reach, and decisioning are connected across the entire P&L – not siloed in adjacent departments that coordinate quarterly.

How to Start Building Your Growth Engine Today

Building the engine does not require perfect conditions. It requires a bias toward action and a willingness to treat organizational design as a growth variable.

The diagnostic: map your failure modes before you build new systems

Before adding new capabilities, identify which of the five failure modes are active in your organization right now. Insight lag and aperture lock are usually structural. Activation gap and decision fog are usually governance failures. Operating model drag requires the deepest intervention. Knowing which failure modes are dominant tells you where to start – and what new systems will fail if you build them on top of an unresolved constraint.

The sequence: what to build first, what to build next

Start with the decisioning layer. Every other component depends on the ability to convert insight into action. A sensing capability without a decision architecture produces analysis paralysis. A reach capability without a decision architecture produces channel proliferation. Get the decision rights clear, the ownership accountable, and the experimentation platform functional before investing heavily in the other four components.

The accountability test: who decides, with what data, by when

Every growth initiative should be able to answer three questions before it moves forward. Who has the authority to decide? What data is required to make that decision with conviction? By when must the decision be made to preserve the opportunity? If any of these three questions cannot be answered clearly, the initiative is not ready to move – and adding more analysis will not fix that.

Frequently Asked Questions

What is a modern growth engine and how is it different from a growth strategy?

A growth strategy defines what to pursue. A modern growth engine is the permanent organizational infrastructure that converts that strategy into compounding action – a sensing layer, a decision architecture, a reach capability, and an accountability structure that learns and improves with each cycle. Strategy is a document. An engine is a system.

Why do enterprise growth initiatives fail even when the strategy is sound?

Most growth initiatives fail not because the strategy is wrong but because the organization lacks the decision architecture to execute it. The five failure modes – insight lag, aperture lock, activation gap, decision fog, and operating model drag – are structural, not strategic. They cannot be resolved by better analysis. They require organizational redesign.

What are the five components of a repeatable enterprise growth engine?

The five components are: human insight (behavioral sensing), growth aperture (horizon-spanning portfolio discipline), customer reach (distribution as strategic infrastructure), the decisioning layer (decision rights and experimentation platforms), and organizational alignment (enterprise-wide accountability and incentive structures). All five must be operational simultaneously for the engine to compound.

How should a mid-market company sequence building its growth engine?

Start with the decisioning layer – clarify who decides what, with what data, by when. Then build the human insight capability to feed that layer with live signals. Reach and aperture expansions are most effective once the decision architecture is functional. Attempting to expand distribution or growth horizons before fixing decision fog typically accelerates the activation gap rather than closing it.

What is the difference between a data problem and a decision problem in enterprise growth?

A data problem means the organization lacks the information needed to act. A decision problem means the information exists but the organization cannot convert it into action – because ownership is unclear, risk tolerance is miscalibrated, or the incentive structures reward inaction. Most enterprises have the former when they actually have the latter. More data does not solve a decision problem.